How I Use Scenarios to Stress-Test Client Portfolios

How I Use Scenarios to Stress-Test Client Portfolios One of the most common assumptions in investing is that the future can be predicted. Investors often rely on forecasts, expert opinions, and market expectations to guide their decisions. However, financial markets are inherently uncertain. Economic cycles shift, geopolitical tensions emerge unexpectedly, and policy decisions can rapidly alter the investment landscape. For this reason, professional portfolio management does not rely on prediction. It relies on preparation. At Income Capital Management, we approach portfolio construction with a clear principle: we do not try to guess the future, we prepare for multiple possible futures. Why Prediction Is Not Enough Traditional investment approaches often depend heavily on forecasts. Analysts predict interest rates, economic growth, inflation trends, and market direction. While these forecasts can provide useful context, they are inherently limited. Markets are influenced by variables that cannot be fully anticipated. Unexpected events—such as geopolitical conflicts, sudden policy shifts, or financial crises—can disrupt even the most well-reasoned predictions. Relying exclusively on a single expected scenario creates vulnerability. If that scenario does not materialize, portfolios can become exposed to significant losses. This is why scenario analysis plays a critical role in modern investment strategy. From Prediction to Preparation Scenario analysis shifts the focus from forecasting a single outcome to evaluating multiple potential environments. Instead of asking, “What will happen?”, the question becomes: “What happens to the portfolio if different things happen?” This approach transforms uncertainty from a threat into a manageable variable. By understanding how a portfolio behaves under different conditions, investors gain clarity, confidence, and control over their financial decisions. The Core Scenarios We Analyze In our portfolio stress-testing process, we model several macroeconomic environments that historically have had a significant impact on financial markets. These scenarios include: Sudden interest rate increases Economic recession or slowdown Inflation shocks Geopolitical instability Liquidity tightening in global markets Each of these environments affects asset classes in different ways. Understanding these relationships is essential for building resilient portfolios. Interest Rate Shock Scenario Interest rates are one of the most powerful drivers of financial markets. A sudden increase in rates can impact equities, bonds, currencies, and real assets simultaneously. In this scenario, we evaluate: Sensitivity of bond and credit exposure Impact on equity valuations Currency adjustments in Forex strategies Real estate financing conditions By modeling these effects, we can identify vulnerabilities and adjust allocations accordingly. Recession Scenario Economic slowdowns or recessions affect corporate earnings, employment levels, and investor sentiment. In a recession scenario, we assess: Equity market drawdown exposure Credit risk in high-yield instruments Liquidity availability Defensive asset allocation effectiveness The goal is to ensure that portfolios maintain stability even in periods of economic contraction. Geopolitical Shock Scenario Geopolitical events—such as conflicts, trade disruptions, or political instability—can introduce sudden volatility into global markets. These events often impact: Currency markets (Forex) Commodity prices Safe-haven assets such as gold Global equity sentiment Scenario analysis allows us to evaluate how portfolios respond to these shocks and whether hedging strategies are sufficient. Inflation and Liquidity Scenarios Inflation dynamics and liquidity conditions are closely linked to central bank policy decisions. These variables influence asset pricing across the entire financial system. We test portfolios against scenarios such as: Persistently high inflation Rapid disinflation Liquidity tightening Expansionary monetary policy Each of these conditions requires different portfolio positioning. Asset Class Behavior Under Stress A key benefit of scenario analysis is understanding how different asset classes behave under stress conditions. For example: Forex strategies may benefit from currency volatility Real estate may provide stability but face financing pressure Equities may experience drawdowns during risk-off periods Gold often acts as a hedge during uncertainty By combining these assets within a diversified framework, portfolios can balance risk and return across different environments. From Analysis to Action Scenario analysis is not just an academic exercise. It directly informs portfolio decisions. Based on the results of stress testing, we may: Rebalance asset allocation Reduce exposure to vulnerable sectors Increase defensive positioning Adjust currency exposure Enhance diversification across asset classes These adjustments are made proactively, rather than reactively. Building Portfolio Resilience Resilience is the ability of a portfolio to withstand shocks while maintaining long-term growth potential. A resilient portfolio does not aim to avoid all volatility. Instead, it is designed to absorb shocks without compromising its long-term trajectory. Scenario analysis plays a central role in achieving this objective. The Psychological Advantage of Stress Testing Beyond technical benefits, scenario analysis provides an important psychological advantage for investors. When clients understand how their portfolio is expected to behave under stress, they are less likely to react emotionally during market turbulence. Confidence comes from preparation. Instead of reacting impulsively to market events, investors can rely on a structured framework that has already considered potential risks. Preparing for Multiple Futures The future will never unfold exactly as expected. Markets will continue to surprise, and new risks will emerge over time. However, by preparing for multiple scenarios, investors can reduce uncertainty and improve decision-making. This approach allows portfolios to remain flexible while maintaining strategic direction. Conclusion Successful investing is not about predicting the future with certainty. It is about building portfolios that can adapt to different outcomes. Scenario analysis transforms uncertainty into a structured process, allowing investors to evaluate risks, adjust exposure, and maintain confidence in their strategy. When you understand how your portfolio behaves under stress, you are better equipped to stay the course—or to adjust with purpose. And in complex financial markets, that clarity makes all the difference. LinkedIn Post:Read the original discussion on LinkedIn

Real Estate Fund: From Bricks to Strategy | Income Capital Management

Real Estate Fund: From Bricks to Strategy By Paolo Volpicelli — Income Capital Management When most people think about investing in real estate, they picture a single property: an apartment to rent out, a commercial unit in a growing city, perhaps a holiday home that doubles as an asset. It is a familiar mental model, and it has served generations of investors reasonably well. But it carries hidden costs that are rarely discussed candidly — concentration risk, illiquidity, management burden, and the kind of idiosyncratic exposure that no amount of local market knowledge can fully insulate you from. At Income Capital Management, we designed our Real Estate Fund on a fundamentally different premise: real estate is not about buying a property. It is about building a strategy. The Problem with Single-Property Investing The appeal of owning a single investment property is understandable. It is tangible, visible, and carries the psychological comfort of something you can walk through and inspect. But from a portfolio construction perspective, a single property is one of the most concentrated positions an investor can hold. Consider what you are actually exposed to when you own one building or one unit. Your returns depend entirely on the performance of a single asset in a single location, often let to a single tenant or a narrow pool of tenants. If the local market softens, if the tenant vacates, if a structural issue emerges, or if regulatory changes affect that specific type of property — the entire investment is impacted. There is no offset, no diversification, no institutional buffer. You bear one hundred percent of a very specific set of risks. Then there is the operational reality. Managing a property — even a single one — requires time, expertise, and ongoing attention. Tenant relations, maintenance, legal compliance, insurance, financing, tax optimization: these are not passive activities. For most investors, the hidden cost of direct property ownership is not just financial. It is the cost of time and mental bandwidth that could be deployed elsewhere. What a Real Estate Fund Actually Provides A professionally managed real estate fund solves the core structural problems of single-property investing by providing something that individual investors almost never have access to on their own: an institutional portfolio. Our Real Estate Fund gives investors exposure to professionally selected projects and assets across diversified tenants and sectors. Rather than concentrating risk in a single building, investors participate in a portfolio that spans different property types — residential, commercial, logistics, hospitality — and different geographies, with each position selected through rigorous due diligence and monitored on an ongoing basis. The difference is not cosmetic. Diversification across tenants and sectors means that the underperformance or vacancy of any single asset has a limited impact on the overall portfolio. A logistics warehouse in one market does not correlate perfectly with a residential development in another. A commercial tenant exiting one property does not create a domino effect across the fund. The portfolio is engineered to be resilient precisely because no single decision, asset, or tenant can determine its fate. This is what we mean when we say we turn bricks into a coherent plan — not isolated decisions. A Strategic Pillar for Investors in Europe, USA and UAE Real estate’s role in a well-constructed portfolio has always been about more than income. It offers three distinct contributions that few other asset classes can replicate simultaneously. Income generation is the most visible benefit. Rental income from a diversified property portfolio provides a relatively stable cash flow stream — one that tends to be less correlated with equity market volatility than dividends or bond coupons. For income-focused investors, particularly those in or approaching retirement, this stability has real value. Partial inflation protection is the second contribution. Property values and rental income have historically shown a meaningful correlation with inflation over medium-to-long time horizons. When the cost of goods and services rises, so do the replacement costs of buildings, the rents that tenants are willing or required to pay, and the nominal value of well-located assets. Real estate is not a perfect inflation hedge — no asset class is — but it provides meaningful protection that pure financial assets often lack. Tangible value is the third pillar. Unlike equities or bonds, a property portfolio is backed by real physical assets with intrinsic utility. People need places to live, work, store goods, and conduct commerce. This demand does not disappear in a financial crisis. The tangible nature of real assets provides a floor under valuations that purely financial instruments do not have, and it gives investors a different kind of psychological anchor during periods of market turbulence. For our clients across Europe, the USA and the UAE, the Real Estate Fund serves as exactly this kind of strategic pillar — a complement to financial assets that provides income, inflation resilience, and asset-backed stability within a broader multi-asset framework. Institutional Access, Professional Management One of the fundamental inequalities of traditional real estate investing is access. The best projects — premium commercial developments, large-scale residential schemes, institutional-grade logistics assets — are not available to individual investors. They require substantial minimum commitments, deep market networks, and the operational infrastructure to manage complex assets across multiple jurisdictions. These are barriers that effectively reserve the highest-quality real estate opportunities for institutional players. Our Real Estate Fund changes this equation. By pooling capital and applying institutional-grade due diligence to asset selection, we give our clients access to the kind of portfolio that would otherwise require tens of millions in direct investment and a dedicated property management team to assemble. Every asset in the fund is selected through a structured evaluation process: market analysis, financial modelling, tenant quality assessment, legal review, and stress testing under adverse scenarios. Every position is monitored continuously, with portfolio-level decisions made by professionals whose full-time focus is exactly this. The investor benefits from this expertise without inheriting the operational complexity that comes with direct ownership. Real Estate Within the Income Capital Framework The Real

Reading Central Banks: A Practical Guide for Investors | Income Capital Management

Reading Central Banks: A Practical Guide for Investors By Nicola Pinchi — Income Capital Management Few forces in global finance move markets as consistently and as broadly as central bank decisions. A single press conference from the Federal Reserve, the European Central Bank, or the Bank of England can reprice bonds across the entire yield curve, send currencies surging or sliding, trigger equity rotations worth hundreds of billions, and shift the risk appetite of institutional investors worldwide — all within the span of a few hours. And yet, for most investors, central bank communication remains one of the most frustrating aspects of financial markets to navigate. The language is deliberately cautious, laden with caveats, and often designed as much to manage market expectations as to convey actual policy intent. After each meeting, headlines compete to offer the definitive interpretation, analysts disagree on the implications, and investors are left wondering what — if anything — they should actually do. At Income Capital Management, we believe the answer is not to react faster to central bank announcements. It is to understand which signals genuinely matter — and to build that understanding into strategic decisions long before the next meeting takes place. Why Monetary Policy for Investors Cannot Be Ignored The influence of central banks on investment portfolios is not a recent phenomenon, but it has become more pronounced in the past two decades. Since the 2008 financial crisis, central bank policy has been the dominant driver of asset valuations across virtually every major market. Ultra-low interest rates and quantitative easing programmes inflated bond prices, compressed credit spreads, boosted equity multiples, and sent real estate values to historic highs. When that cycle eventually reversed — as it did sharply from 2022 onwards — the damage across asset classes was equally broad. Understanding the direction of monetary policy is therefore not an academic exercise for macroeconomists. It is a practical necessity for anyone managing a diversified portfolio. Whether you hold bonds, equities, currency positions, or real assets, the path of interest rates and central bank liquidity conditions will influence your returns, your risk profile, and your optimal asset allocation in ways that no bottom-up analysis of individual securities can fully compensate for. The challenge is not recognising this fact. The challenge is developing a systematic, repeatable framework for extracting actionable insight from the noise of central bank communication — without getting lost in every nuance of every statement. The Four Signals That Actually Matter Over years of integrating monetary policy analysis into portfolio management across Forex, High Yield, Global Growth and Real Estate, we have found that four signals consistently carry the most predictive weight. Everything else is largely commentary. Inflation trends are the bedrock. Central banks exist primarily to manage price stability, and their policy decisions are ultimately a response to what inflation is doing and where it is expected to go. When inflation is rising above target, the policy bias will lean restrictive — higher rates, tighter liquidity conditions, a headwind for duration-sensitive assets. When inflation is falling towards or below target, the bias shifts accommodative. Tracking the evolution of core inflation, services inflation, and inflation expectations — rather than headline CPI alone — gives a far more reliable read on the direction of travel than any central bank statement. Policy direction and pace matter as much as the absolute level of rates. Markets do not reprice because rates are high or low in absolute terms; they reprice when the direction or pace of change surprises. A central bank that signals it is done hiking — even at elevated rates — is providing a very different environment for risk assets than one that is actively tightening. Learning to identify genuine policy pivots, as distinct from tactical pauses or communication management, is one of the most valuable skills a macro-aware investor can develop. Liquidity conditions are the transmission mechanism that connects monetary policy to real market behaviour. Beyond the policy rate itself, the size and composition of central bank balance sheets, the pace of quantitative tightening or easing, and the functioning of repo and money markets all determine how easily credit flows through the financial system. Periods of ample liquidity tend to compress risk premiums and support asset prices. Periods of tightening liquidity have the opposite effect — often before the impact shows up in economic data. Monitoring these conditions provides an early warning system that pure rate analysis misses. Central bank credibility is the most intangible of the four signals, but ultimately the most powerful. A central bank that the market believes will do what it says — that has a track record of hitting its inflation target, communicating consistently, and following through on its commitments — has enormous capacity to stabilise expectations without dramatic policy action. A central bank that has lost credibility, or that sends confused signals, generates persistent uncertainty that increases volatility across all asset classes. Assessing credibility requires a qualitative overlay on top of quantitative data, but it is essential to getting the framework right. From Analysis to Portfolio Decisions Understanding these four signals is necessary. Knowing how to translate them into portfolio positioning is what makes the analysis useful. In our Forex strategies, monetary policy divergence between central banks is the primary driver of medium-term currency moves. When the Fed is tightening while the ECB is on hold, or when the Bank of Japan is normalising while the Bank of England is cutting, these differentials create directional Forex opportunities that can be captured systematically. The key is distinguishing between divergences that are already priced in and those that the market has not yet fully discounted. In our High Yield credit allocations, the liquidity cycle is particularly critical. Loose monetary conditions compress spreads and reduce default risk by making refinancing easier for leveraged borrowers. Tightening conditions have the opposite effect: spreads widen, refinancing becomes more expensive, and the weakest credits face genuine stress. Mapping the liquidity cycle allows us to adjust credit quality and duration positioning well

How I Explain Investment Risk to Non-Finance People | Income Capital Management

How I Explain Investment Risk to Non-Finance People By Paolo Volpicelli — Income Capital Management Risk is the most important concept in finance. It is also the one most consistently explained badly. When investment professionals talk about risk with each other, they speak in the language of standard deviations, Value at Risk, Sharpe ratios, and maximum drawdown percentages. This language is precise and useful — among professionals. But when a surgeon, a family business owner, a lawyer, or a parent sits across the table from you and asks “is this safe?”, that vocabulary does not just fail to help. It actively gets in the way. Over years of working with clients from backgrounds far outside finance at Income Capital Management, I have learned that the goal of a risk conversation is not to educate people about financial theory. It is to connect what the numbers mean to what the person actually feels, needs, and fears. That requires a completely different approach — and a completely different set of questions. Investment Risk Explained: Start With Questions, Not Definitions The single most effective tool I have found for explaining investment risk is not a chart, not a formula, and not a slide deck. It is a question. Specifically, three questions that I ask every new client before we discuss a single number: “How would you feel if your portfolio dropped 15% in one year?” Not: what is your risk tolerance on a scale of one to ten. Not: are you a conservative, balanced, or aggressive investor. Those abstract categories produce abstract answers that do not survive contact with a real drawdown. Asking how someone would feel — not what they would think — opens a completely different conversation. Some people say “I would be worried but I would hold on.” Others say “I would not be able to sleep.” Both answers are equally valid, and both tell me something essential about how a portfolio needs to be designed. “How stable is your income?” A surgeon with a long, established practice has very different risk capacity than a freelancer whose revenues swing significantly from year to year, even if both have the same amount to invest. Risk capacity — the financial ability to absorb losses without being forced to sell at the wrong moment — is as important as risk tolerance, and it is almost always determined by the stability and predictability of the client’s income and obligations outside the portfolio. “What is non-negotiable for your family?” Every client has a financial floor — a level below which their lifestyle, their family’s security, or their business cannot function. Identifying that floor explicitly is what allows us to design a portfolio that can pursue growth or income above it while protecting the capital that is genuinely irreplaceable. This question makes the abstract concept of capital preservation concrete and personal. From Emotions to Numbers: Translating Risk Into Reality Once these questions have been answered, something important has happened: the client has connected their emotional reality to the financial decisions ahead. At that point, introducing technical concepts becomes not only possible but natural — because they now have a personal frame of reference to attach them to. Volatility is the measure of how much a portfolio value fluctuates over time. For most non-finance clients, this becomes meaningful the moment you link it back to their first answer: “a portfolio with this level of volatility might drop 15% in a bad year, but it has historically recovered within two to three years.” Suddenly volatility is not an abstract statistical concept — it is the price of participation in a strategy that delivers a specific long-term return. Drawdown — the peak-to-trough decline in portfolio value — is the concept that tends to land hardest when clients experience it for the first time. The reason is that a 20% loss requires a 25% gain just to break even: the mathematics of loss are asymmetric, and most people have not internalised this intuitively. I explain this not with formulas but with simple examples: “if you invest 100 and it drops to 80, you need to grow from 80 back to 100, which is a 25% return from that lower base.” That single insight changes how people think about managing the downside. Liquidity is perhaps the risk that surprises non-finance clients most when they encounter it in practice. The idea that an investment might be performing well but simply not be accessible when needed — because of redemption windows, lock-up periods, or illiquid market conditions — is counterintuitive to people accustomed to a current account or a savings product. I explain liquidity through the lens of their third question: if something non-negotiable for your family required €50,000 in the next three months, could we access it without disrupting the rest of the strategy? That question makes liquidity risk immediately real. Time horizon is the variable that ties everything else together. A short time horizon transforms risks that are perfectly manageable over ten years into genuine threats — because there is no time for recovery. Aligning the investment strategy with the client’s actual time horizon for each pool of capital is one of the most impactful decisions in portfolio construction, and one that only becomes possible when the client has been genuinely honest about what different parts of their wealth are for. When People Understand Risk, Returns Become a Consequence The most important shift I have observed in clients who have gone through this kind of risk conversation is not technical. It is psychological. Before the conversation, most people approach investing primarily through the lens of returns: what will this make me? After a genuine, grounded risk conversation, the frame changes: what can I hold through, and what will that enable over time? This shift matters enormously for long-term investment outcomes. Investors who understand the risks they are taking — and who have chosen those risks deliberately, in line with their real emotional and financial capacity — are far more likely

Physical Gold Investment: More Than Just a Safe Haven | Income Capital Management

Physical Gold Investment: More Than Just a Safe Haven By Paolo Volpicelli — Income Capital Management Ask most investors what gold is for, and you will hear the same answer: it is something you hold when everything else is going wrong. A crisis asset. A last resort. The thing you turn to when currencies collapse, markets implode, or geopolitical risk spikes beyond what conventional portfolios can absorb. This view of gold is not wrong — but it is incomplete, and for many investors it leads to a systematic underuse of one of the most versatile assets available in modern portfolio construction. Physical gold has been a store of value for thousands of years. That track record is real and it matters. But for today’s investor, the question is not whether gold has preserved wealth across centuries. The question is whether it belongs in your portfolio right now — in what form, in what size, and connected to what overall strategy. At Income Capital Management, our answer is yes — and the reasoning goes well beyond the traditional safe-haven narrative. Why Physical Gold Investment Still Makes Sense Gold has outlasted every fiat currency ever created. That single fact carries more weight than any quantitative model, because it reflects something fundamental about the nature of the asset: it cannot be printed, debased, or defaulted on. In a world where central bank balance sheets have expanded to historic proportions and sovereign debt levels in major economies continue to rise, this property is not merely historical — it is structurally relevant. But the case for physical gold investment in a modern portfolio rests on more than distrust of paper money. Gold has several concrete portfolio characteristics that make it genuinely useful as an active strategic allocation rather than a passive emergency reserve. First, gold has a low and sometimes negative correlation with equities and credit assets during periods of acute market stress — precisely when diversification from traditional assets matters most. When equity markets sell off sharply and credit spreads widen, gold often moves in the opposite direction, providing a natural offset to losses elsewhere in the portfolio. This is not a coincidence; it reflects gold’s role as a preferred destination for capital during risk-off regimes. Second, gold has historically maintained its purchasing power over long periods relative to goods and services. While it is not a perfect inflation hedge in the short term — gold can underperform for extended periods even when inflation is elevated — over multi-decade horizons it has consistently preserved real value in ways that nominal bonds and cash cannot. For investors with long time horizons and a concern about the erosion of purchasing power, this is a meaningful contribution. Third, and perhaps most importantly for portfolio construction purposes, gold provides psychological stability. During periods of severe market stress, investors with a meaningful gold allocation tend to behave more rationally — because they can see a portion of their wealth holding its value or appreciating while other assets fall. This behavioural dimension is underrated in academic portfolio theory but critical in practice. An investor who stays invested through a crash because their gold allocation is cushioning the drawdown will almost always outperform one who sells everything at the bottom. Allocated Holdings: Why Physical Matters Not all gold exposure is equivalent, and the distinction between physical gold and paper gold is one that every serious investor should understand clearly. Gold ETFs, futures, and certificates offer convenient price exposure to gold — but they are financial instruments, not the metal itself. In a genuine tail risk scenario — the kind of systemic stress that gold is most valued for hedging against — the performance of these instruments depends on the functioning of the financial infrastructure that underlies them: clearing houses, counterparties, custodians, and markets. In extreme scenarios, that infrastructure is precisely what may be under strain. Allocated physical gold holdings are different. When gold is held in allocated form, specific bars or coins are legally assigned to the investor and segregated from the custodian’s own assets. The investor owns the physical metal — not a claim on it, not exposure to it, but the metal itself — held on their behalf in a professional custody facility with independent auditing and transparent pricing. Through our Physical Gold solution at Income Capital Management, clients access exactly this structure: allocated holdings with professional custody, independently verified, fully transparent in pricing, and fully integrated into their broader portfolio reporting. The gold they hold is real, auditable, and legally theirs — with none of the counterparty risk that attaches to paper alternatives. Sizing and Integration: The Key to Making Gold Work The most common mistake investors make with gold is not holding it — it is holding it wrong. Specifically, treating it as an isolated position rather than a deliberately sized component of an integrated strategy. Too little gold — a token 1% or 2% allocation added almost as an afterthought — provides negligible diversification benefit. It is large enough to require management attention but too small to meaningfully offset losses in other assets during a crisis. Too much gold — a concentrated 20% or 30% allocation driven by macro anxiety — creates a different problem: gold generates no income, pays no dividend, and produces no cash flow. An overweight gold position is a bet on continued monetary instability, and while that bet may eventually pay off, it extracts a significant opportunity cost in the interim. The right allocation depends on the client’s broader portfolio, their income requirements, their time horizon, and their specific exposure to the risks that gold is most effective at hedging. For most diversified portfolios, a strategic allocation in the range of 5% to 10% tends to capture the meaningful diversification and tail-risk hedging benefits of gold without sacrificing too much in terms of income generation or growth potential. Crucially, this allocation needs to be connected to the overall strategy — not treated as a standalone bet. In our framework, the Physical

Love Your Investments: Building Lasting Relationships with Your Portfolio

Love Your Investments: Building Lasting Relationships with Your Portfolio Valentine’s Day is often associated with romantic symbolism — flowers, promises, and grand gestures. In finance, the word “love” may seem misplaced. Yet the concept of lasting commitment, patience, and mutual understanding has surprising relevance in the world of long-term investing. Portfolios, like relationships, thrive not because of intensity, but because of consistency. The Myth of Instant Attraction in Investing Many investment decisions begin with excitement. A new fund, a promising sector, an emerging market opportunity — each carries the appeal of novelty. Just as in relationships, initial enthusiasm can create a powerful emotional pull. However, history repeatedly shows that sustainable wealth is not built on short-term excitement. It is built on structured commitment. Markets reward patience more reliably than impulsiveness. A portfolio that constantly changes direction in pursuit of the next opportunity rarely develops depth or resilience. Commitment as Strategic Discipline Commitment in investing does not mean blind loyalty to underperforming assets. It means adhering to a structured allocation framework through market cycles. At Income Capital Management, disciplined commitment manifests in: Defined asset allocation ranges. Regular review processes. Transparent communication during volatility. Measured rebalancing rather than emotional repositioning. This approach mirrors a long-term partnership. Both sides understand that fluctuations occur, but structure provides stability. Trust Between Advisor and Client In relationships, trust is cumulative. It develops through transparency and shared expectations. The same principle governs advisor-client dynamics. Clients who understand the purpose of each allocation — Forex, Real Estate, Physical Gold, Global Growth, High Yield — are less vulnerable to fear-driven decisions. Trust reduces reactive behavior. It creates psychological resilience. Regular Engagement Prevents Drift Relationships deteriorate when communication fades. Portfolios suffer similarly when left unattended. Periodic portfolio reviews serve multiple purposes: Reaffirming long-term goals. Adjusting for life changes. Rebalancing allocations to maintain strategic alignment. Reassessing risk tolerance. Without engagement, portfolios drift from original objectives — not because markets fail, but because circumstances evolve. Understanding Volatility as Emotional Testing Volatility is the emotional test of every investor. Market drawdowns feel personal. Headlines amplify uncertainty. Yet volatility is not betrayal. It is a structural feature of capital markets. When investors internalize this reality, they stop perceiving temporary underperformance as failure. Instead, they evaluate whether the original thesis remains intact. Mutual Responsibility Successful advisory relationships are collaborative. Advisors provide structure, analysis, and risk frameworks. Clients provide clarity regarding goals, time horizon, and liquidity needs. When both roles are respected, outcomes improve. Long-Term Wealth Is Emotional Stability Beyond financial metrics, disciplined portfolio relationships cultivate psychological stability. Investors who trust their framework experience less anxiety during market turbulence. Emotional stability enhances decision quality. Love the Process, Not the Outcome Focusing exclusively on short-term performance is analogous to evaluating a relationship solely on daily mood fluctuations. Long-term investing requires appreciation of process — risk management, diversification, scenario analysis — rather than obsession with quarterly returns. The Role of Patience Compounding requires time. Time requires patience. Patience requires conviction. Conviction arises from understanding. When investors fully understand their portfolio structure, patience becomes rational rather than forced. Conclusion: Stability Through Commitment Lasting wealth is built through sustained engagement, structured discipline, and trusted partnership. Just as enduring relationships are grounded in respect and shared values, enduring portfolios are grounded in clarity, risk awareness, and long-term alignment. In investing, as in life, love is not intensity. It is commitment sustained over time. LinkedIn Post: https://www.linkedin.com/posts/incomecapital_portfolio-commitment-investments-activity-7427985167228579840-Pg5d

Entrepreneurship and Finance: Lessons from Building Income Capital Management

Entrepreneurship and Finance: Lessons from Building Income Capital Management When people think about finance, they often imagine numbers, models, and capital markets. When they think about entrepreneurship, they imagine innovation, ambition, and risk-taking. In reality, these two disciplines are deeply interconnected. Building Income Capital Management has reinforced a conviction I now hold with certainty: serious investing is an entrepreneurial act. An investment firm is not simply a vehicle for deploying capital. It is an enterprise built on vision, execution, regulatory structure, human relationships, and disciplined risk management. The parallels between launching a company and constructing resilient portfolios are more profound than they appear at first glance. Vision Is the First Allocation Decision Every entrepreneurial journey begins with a vision. In finance, that vision must extend beyond returns. It must define purpose. When we designed the foundations of Income Capital Management, the initial question was not “How do we outperform this year?” but rather “What type of institution do we want to be ten or twenty years from now?” That framing changed every subsequent decision. Vision in finance determines: The type of clients you serve. The jurisdictions you operate in. The level of regulatory compliance you adopt. The risk profile you are willing to manage. The balance between innovation and prudence. Without a long-term institutional vision, short-term performance can become dangerously seductive. Entrepreneurs learn that misaligned growth can destroy stability. Investors face the same reality. Execution Is Where Trust Is Built Ideas are abundant in financial markets. Execution is scarce. Launching a Forex strategy, structuring a Real Estate vehicle, integrating Physical Gold custody, implementing High Yield allocations, building Global Growth frameworks — none of these are inherently complex ideas. What differentiates sustainable institutions from temporary ones is execution discipline. Execution in finance includes: Risk management protocols. Transparent reporting. Regulatory adherence. Liquidity monitoring. Client communication standards. Entrepreneurship taught me that credibility is operational. In wealth management, operational weakness translates directly into reputational risk. Regulatory Expansion as Strategic Maturity One of the most underestimated lessons in financial entrepreneurship is the importance of regulatory evolution. Expanding into new jurisdictions, adapting to cross-border frameworks, and strengthening compliance infrastructure are not bureaucratic burdens — they are strategic investments. Each regulatory milestone required capital, time, and organizational adaptation. But every expansion strengthened the institutional foundation and enhanced client confidence. Entrepreneurship in finance is not about avoiding structure. It is about building robust structure. Adaptability Without Instability Markets evolve. Economic regimes shift. Monetary cycles reverse. Technology transforms distribution channels. Regulation tightens. An investment firm must adapt — but adaptation must not compromise identity. Over time, we adjusted risk limits, refined asset allocation models, expanded into additional strategies and improved data integration. Yet the core philosophy remained intact: disciplined diversification, transparent advisory, and long-term alignment. Entrepreneurs face a similar tension: adapt to survive, but do not drift without direction. Client Obsession as Institutional Strategy In many industries, “customer focus” is a marketing phrase. In wealth management, it is existential. Capital is mobile. Trust is fragile. Performance alone does not secure loyalty. Clients remain committed when they understand what they own, why they own it, and how it behaves under stress. This requires: Clear risk explanation. Scenario transparency. Alignment between portfolio design and life goals. Honest communication during drawdowns. Entrepreneurial growth followed when clients felt understood, not impressed. Resilience as a Core Asset No serious entrepreneur avoids downturns. Likewise, no serious investor avoids volatility. The early years of building an investment firm are characterized by limited margin for error. Every drawdown feels amplified. Every operational challenge tests conviction. Resilience became not just a psychological trait, but a structural design principle. Diversification across strategies was not simply a client benefit — it was an institutional safeguard. Timing and Optionality Entrepreneurs rarely possess perfect information. Decisions are made under uncertainty. The same is true in investing. Waiting for perfect clarity often results in missed opportunity. Acting without preparation leads to unnecessary risk. The balance lies in optionality — maintaining liquidity, flexible structures, and scenario-tested frameworks that allow participation without overcommitment. Growth as a Controlled Process Scaling an investment firm resembles scaling a business. Rapid expansion without infrastructure can destabilize operations. We deliberately prioritized controlled growth. Technology upgrades preceded distribution expansion. Risk systems evolved before asset size increased materially. In investing, position sizing plays the same role. Growth must be proportionate to risk capacity. The Entrepreneurial Mindset in Portfolio Construction Every investor is, in effect, managing a financial enterprise. Asset allocation mirrors strategic planning. Liquidity resembles operational cash flow. Risk tolerance parallels competitive positioning. When investors begin to see their portfolio as a business rather than a collection of products, decision quality improves. Long-Term Value Creation Over Excitement Financial markets reward patience more reliably than excitement. Entrepreneurship reinforced that sustainable institutions are built quietly. Similarly, sustainable portfolios are constructed through disciplined processes rather than dramatic moves. The lessons from building Income Capital Management extend beyond corporate structure. They reveal that finance, at its highest level, is entrepreneurship applied to capital. Vision, execution, adaptability, discipline, and client alignment — these principles govern both worlds. And in both worlds, longevity is the ultimate measure of success. LinkedIn Post: https://www.linkedin.com/posts/paolovolpicelli_finance-investment-vision-activity-7427282770026070016-4rkS

PRESS RELEASE – TEARLY RESULTS 2025

Income Capital Management Reports Strong 2025 Performance in a Year of Divergent Global Markets FOR IMMEDIATE RELEASE Date: January 27, 2026 Prague, Czech Republic — Income Capital Management closed 2025 with solid results across its diversified investment strategies, successfully navigating a year marked by sharp divergences between asset classes. The firm enters 2026 with a disciplined, multi-asset approach focused on delivering consistent value to its investors. Market Environment Global markets in 2025 were characterized by pronounced dispersion. Gold emerged as the top-performing major asset class, posting gains of +65.87% and reinforcing its role as a safe-haven asset. Major equity indices, including DAX, NASDAQ, FTSE 100, Euro Stoxx 50, S&P 500, and Dow Jones, recorded positive performances, while Bitcoin declined by -6.35%, reflecting increased volatility and speculative risk. Italy’s FTSE MIB underperformed relative to broader international benchmarks. Key Strategy Performance Income Capital Management’s Forex strategy delivered a standout performance, achieving an annual return of +34.98%. Active currency trading combined with strict risk management allowed the strategy to outperform major traditional benchmarks. The firm’s Real Estate strategy generated stable income-driven returns of +7.71%, supported by premium property assets and consistent cash flow, outperforming several weaker regional equity markets. Additional allocations to global growth and high-yield strategies contributed to overall portfolio diversification and balance. Management Commentary “2025 confirmed that active and diversified strategies are essential in fragmented market conditions,” said Paolo Volpicelli, CEO of Income Capital Management. “Our Forex strategy’s 34.98% return demonstrates how disciplined execution and controlled risk can translate into meaningful performance for our investors.” Nicola Pinchi, CTO of Income Capital Management, added: “By combining high-conviction Forex strategies with stable real estate income and physical gold exposure, we have built portfolios designed to perform across different market cycles rather than simply follow short-term trends.” Strategic Positioning for 2026 Income Capital Management’s multi-asset framework — encompassing Forex for growth, real estate for income, global growth and high-yield strategies for diversification, and physical gold for capital protection — is designed to provide resilience and flexibility in an evolving macroeconomic environment. As the firm enters 2026, this structure aims to balance opportunity and risk, supporting long-term portfolio stability in periods of heightened volatility. About Income Capital Management Income Capital Management is an independent asset management firm specializing in diversified investment solutions across Forex, real estate, global growth, high-yield strategies, and physical asset exposure. The firm focuses on active management, disciplined risk control, and long-term capital preservation and growth. For more information, please visit www.incomecapital.biz or contact the Income Capital Management team directly. LinkedIn press release: https://www.linkedin.com/posts/paolovolpicelli_press-release-tearly-results-2025-activity-7421816797093494784-NoVd

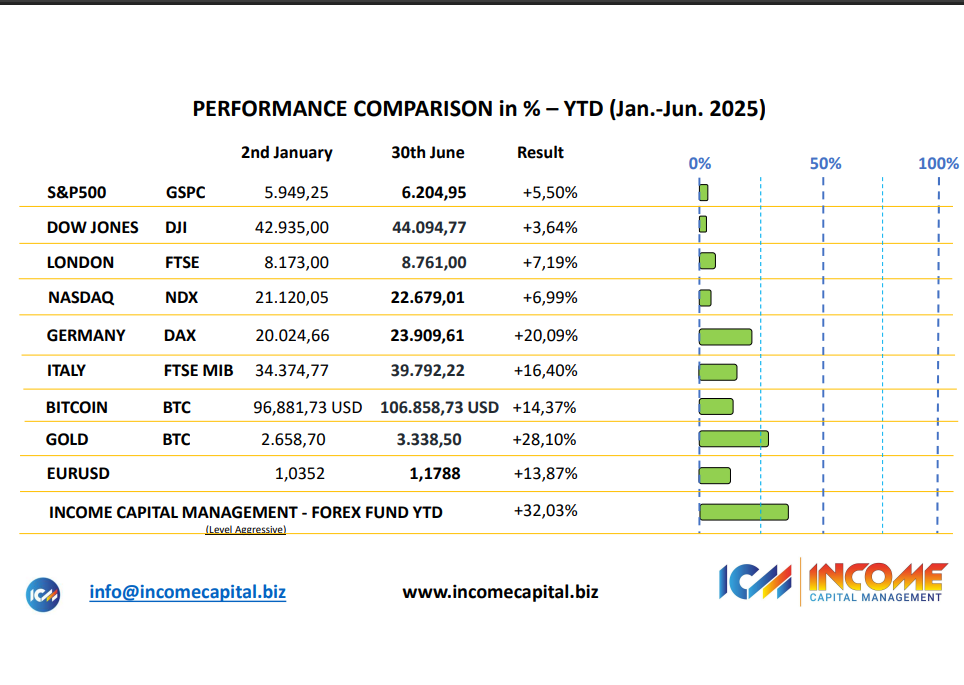

INCOME CAPITAL MANAGEMENT Shines in H1 2025: Performance, Discipline, and Conviction

INCOME CAPITAL MANAGEMENT Shines in H1 2025: Performance, Discipline, and Conviction The first half of 2025 has been anything but simple for global financial markets. Persistent geopolitical tensions, fluctuating monetary policies, and ongoing macroeconomic uncertainty have created an environment where consistency and discipline matter more than bold predictions. Against this backdrop, INCOME CAPITAL MANAGEMENT delivered a solid and measurable result, confirming the robustness of its investment framework and the effectiveness of its risk-controlled execution. 📊 Strong Performance in a Challenging Environment During the first half of 2025, our Aggressive Investment Level achieved: +32.03% cumulative return (H1 2025) +62.08% cumulative return since April 2024 These figures are not the result of isolated market events or short-term positioning. They reflect a structured and repeatable investment process built around: Disciplined FX strategy execution Dynamic exposure management Continuous risk monitoring and adjustment Data-driven decision-making Past performance refers to the Aggressive Investment Level and is not indicative of future results. 📌 Structure Over Speculation As highlighted by our Founder & CEO, Paolo Volpicelli, performance is not driven by luck: “Our edge is not luck — it is structure, conviction, and execution.” At INCOME CAPITAL MANAGEMENT, we do not attempt to predict markets. Instead, we focus on understanding them, adapting to changing conditions, and maintaining a disciplined framework that prioritizes capital preservation alongside growth. In an environment where many strategies struggle to remain consistent, our approach continues to demonstrate resilience through methodical positioning and controlled risk exposure. 🔍 Transparency and Measurable Results We believe that performance should always be: Measurable – backed by real data Transparent – clearly reported and accessible Consistent – aligned with a defined investment process Our results reflect not only market opportunities but also the strength of a framework designed to operate effectively during both expansionary and volatile phases. 🔗 Further Insights For the original update and additional context, you can view the LinkedIn article here: View the original LinkedIn post → 🧠 Looking Ahead The first half of 2025 reinforces a key principle: in complex markets, conviction and consistency outperform noise and reaction. As we move into the second half of the year, our focus remains unchanged — protecting capital, managing risk intelligently, and delivering sustainable performance through disciplined execution. INCOME CAPITAL MANAGEMENT continues to build results through structure, not shortcuts.

INCOME CAPITAL FOREX FUND – Questions & Answers (April 2024)

INCOME CAPITAL FOREX FUND – Questions & Answers (April 2024) What is the INCOME CAPITAL FOREX Fund? The INCOME CAPITAL FOREX Fund is an investment fund managed by INCOME CAPITAL MANAGEMENT s.r.o. that operates in the global foreign exchange (FX) market. Its objective is capital appreciation through active currency trading using a structured and risk-controlled approach. What does the Fund invest in? The Fund trades major currency pairs, primarily: EUR/USD EUR/GBP GBP/USD Trading activity is focused on liquid FX markets, allowing efficient execution and continuous risk monitoring. What is the investment objective of the Fund? The objective is to generate returns through active forex trading while applying disciplined risk management. The Fund does not aim to guarantee profits and does not eliminate market risk. What type of strategy does the Fund use? The Fund adopts an active trading strategy with a scalping-oriented approach, meaning it takes advantage of short-term price movements in the currency markets. Investment decisions are supported by: Fundamental analysis (macroeconomic data, interest rates, geopolitical events) Technical analysis (price patterns, market behavior) Technology-supported execution systems Does the Fund use Artificial Intelligence? Yes. The Fund uses AI and algorithmic tools to support market analysis and trade execution. AI is used to: Analyze large datasets of historical and live market data Identify patterns and market signals Support decision-making and execution efficiency AI does not operate independently and is always subject to human oversight and risk controls. Who manages the Fund? The Fund is managed by professional fund managers supported by financial analysts, automated trading systems (Expert Advisors), and risk management and compliance teams. Human supervision remains central to the investment process. What is the risk level of the Forex Fund? The Forex Fund has a medium-to-high risk profile. Foreign exchange markets are volatile, and losses can occur, including partial or total loss of invested capital depending on the investment level chosen. What are the main risks involved? Key risks include: Market and volatility risk Currency risk Liquidity risk Technological and system risk Operational and regulatory risk Investors should carefully assess their risk tolerance before investing. How does the Fund manage risk? Risk management measures include position sizing rules, stop-loss mechanisms, continuous monitoring of market exposure, diversification of trading positions, and compliance with regulatory standards. Risk is actively managed but cannot be eliminated. Are there different investment levels? Yes. The Fund offers four investment levels: Conservative – lower risk, partial capital protection, lower return range Mild-Conservative – balanced approach between risk and protection Mild-Aggressive – higher risk with higher potential returns Aggressive – highest risk and highest return potential Each level has a defined expected return range and capital protection structure, where applicable. Is capital guaranteed? Capital protection depends on the selected investment level. Some levels offer partial capital protection, while others are fully exposed to market risk. Capital is never fully guaranteed. How often are returns updated? Returns are updated weekly for the Forex Fund. Performance is calculated based on the working amount invested. Returns may vary depending on market conditions. What fees apply to the Forex Fund? There are no entry fees and no fixed management fees. A performance fee is applied only on realized net profits. Compliance-related onboarding costs (KYC/AML) are borne by the investor. Can an investor exit before maturity? Yes. Early exit is possible under predefined conditions. Fees or penalties may apply depending on the investment level, duration of the investment, and timing of the withdrawal. Details are specified in the official documentation. Who can invest in the Forex Fund? The Fund is intended for investors who understand financial markets and FX trading risks, are comfortable with medium-to-high risk investments, and have a medium to long-term investment horizon. The Fund may not be suitable for all investors. Is the Fund regulated? Yes. INCOME CAPITAL MANAGEMENT s.r.o. operates under the supervision of the Czech National Bank, in accordance with applicable regulations. All investors are subject to KYC, AML, and PEP checks. How is transparency ensured? Transparency is ensured through regular performance reporting, access to investment data via the private client area, dedicated investor support, and clear documentation outlining risks, fees, and strategy. Where can investors find official documentation? Official documentation, including the KID, is provided during onboarding and is available upon request from INCOME CAPITAL MANAGEMENT. Is this information investment advice? No. This information is provided for educational and informational purposes only and does not constitute investment advice. Investors should seek independent professional advice before making any investment decision.